We originally posted this blog on The Whitecoat Investor, but have provided it here as well:

The last two years has seen inflation climb to levels not seen this century . The Consumer Price Index (CPI) was 8.6 in 2022, over four times the average, and the CPI was 4.7 for 2021, over twice the average. Now is the time to thoroughly examine the merits of the Cost-of-Living Adjustment Rider (COLA). To review, the COLA rider is an optional rider that increases the base monthly benefit of a disability insurance policy. So far, so good, but let’s look deeper. This rider only becomes active once you have filed a claim and have been receiving benefits for 12 months. Each company is different in how much extra benefit they provide and the rules for how they calculate it, and extra premium is charged to add the rider. Should a COLA rider be added to your next or current disability insurance policy? If the insurance companies included this rider for no extra premium the decision would be easy. Why would you not want your monthly benefit to keep pace with inflation? Unfortunately for the consumer, insurance companies are experts at assessing risk and levying the premium required to insure that risk, and COLA is no different. In this article we will study the costs of COLA, the benefits, and provide the data for you to make an informed decision.

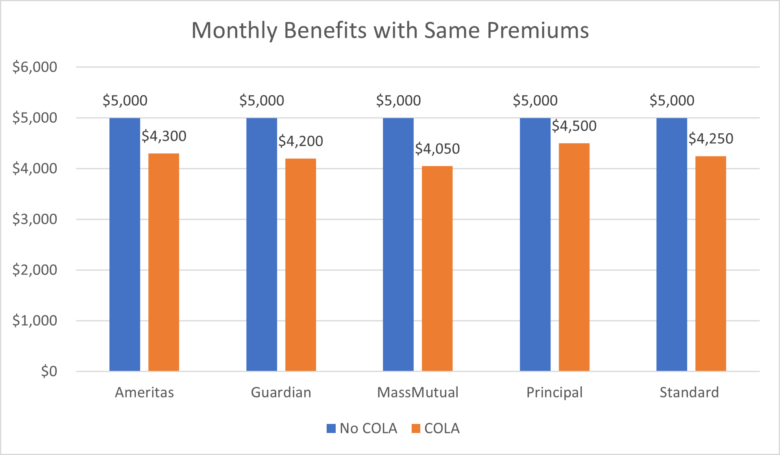

For this study we obtained illustrations from Ameritas, Guardian, MassMutual, Principal and Standard for male and female rates at ages 30,35, and 40 for various states. We used various medical specialties and occupational classes and illustrated a $5,000 per month benefit with a benefit period of age 67 and a 90-day elimination period. To make this as accurate as possible, we wanted to simulate the real life everyday policies physicians are requesting and obtaining, so we added enhanced residual/partial benefits. Some companies include FIO, but not all, so we did not add if not automatically included. We ran these both with and without COLA to gauge the premium differences. We ran all illustrations with California rates and policy provisions and compared them against New York and Texas rates to make sure the cost differential was the same with all carriers, which we found out be true. We then reduced the monthly benefit for the policy with COLA to equal the premium of the $5,000 monthly benefit without COLA. Since each company has a different way to calculate how they pay the COLA increase we used the following from each company for our study:

· Ameritas: 3% simple annually, regardless of CPI

· Guardian: 3% compounded annually, regardless of CPI

· MassMutual: 3% compounded annually, regardless of CPI

· Principal: Up to 3% compounded annually, depending on performance of CPI. Negative or flat CPI will result in a 0% change, and anything above 3% will be capped at 3%.

· Standard: Up to 3% compounded annually, depending on performance of CPI. Negative or flat CPI will result in a 0% change, and anything above 3% will be capped at 3%.

Since each age, gender, and specialty produced virtually the same percentage premium differential between premiums with and without COLA we used a 35-year-old male invasive physician as our case study subject with California rates and level premiums. We then reduced the monthly benefit for the policy with COLA to equal the premium of the $5,000 monthly benefit without COLA. which resulted in the following:

** Based on equal premiums paid with and without COLA for each company, however we did not adjust for the premium differences between companies.

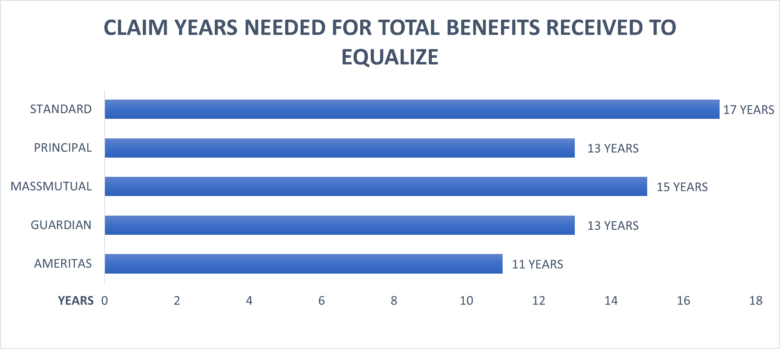

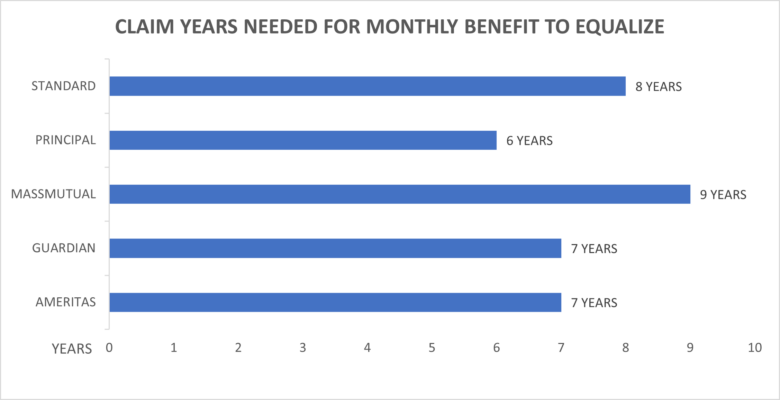

We then used the linked CPI-U chart, taken from the Federal Reserve Bank of Minneapolis. From this chart we took data from the last 23 years, which we felt would be the most pertinent, and averaged it out to 1.925%. Since with all carriers the cap increase is 3% (some carriers offer a higher cap percentage, but for the purposes of our study we only used the 3% cap premium), for the six years that the CPI exceeded 3%, we only used 3% for the average calculation. As noted above, some carriers guarantee 3% while others follow the CPI, since that was the most a carrier would pay each year. Our final calculation determines the number of years an insured will have to be on claim to receive equal payments to someone without COLA who is also

on claim. We assumed with each policy that benefits would be paid and ignored any differences in any other contractual provisions. We also did not take into consideration the time value of money that would make receiving the extra funds sooner much more valuable.

The following charts indicate the number of years on claim for the monthly benefits of the COLA policy to equal the original $5,000 per month policy, and also the number of years for the total claim amount received to equalize, based on the CPI of this century. Take note if the average CPI is lower than 1.925% equalization would be longer and if the CPI average was more it would be shorter.

Since the premium expenditure is equal each physician should determine if they want the additional benefits immediately upon claim or deferred in the future. Our claims experience points to higher benefits sooner when the shock of lower income is greater than later when an individual has had time to plan and adjust for lower income.

Based on our research it is preferable to increase the monthly benefit in lieu of adding a COLA rider. This is reinforced by the fact that insurance companies settle most long-term disability claims with a lump sum settlement. There are some instances when it may be advisable to obtain the maximum monthly benefit available and add the COLA rider, such as when a physician is in the military and has limited monthly benefit in relation to income. A physician can always remove the COLA rider in the future and increase the monthly benefit at that time.

We encourage your comments.

Andy Borgia, CLU

DK Unger

858-523-7572

info@di4mds.com